SOL 11a: How do people deal with scarcity, resources, choice, opportunity cost, price, incentives, supply and demand, production, and consumption?

People make choices about how to use limited

resources, decide the ownership of resources, and structure markets for the

distribution of goods and services.

Scarcity is the inability to satisfy all wants at the same time. All resources and goods are limited. This requires that choices be

made. EX: A baker may only have enough dough to make bread, croissants, or bagels, and must decide which option is best.

Resources are factors of production that are used in the

production of goods and services. Types of resources are natural (trees, oil), human (workers), capital (tools, cash registers), and entrepreneurship (business owners, inventors).

Choice is selection of an item or action from a set of possible alternatives. Individuals must choose or make decisions about desired goods and services because these goods and services are limited.

Opportunity cost is what is given up when a choice is made—i.e., the highest valued alternative is forgone. Individuals must consider the value of what is given up when making a choice. EX: If you want to buy a book and a game, but you only have enough for one, the one you give up is the opportunity cost.

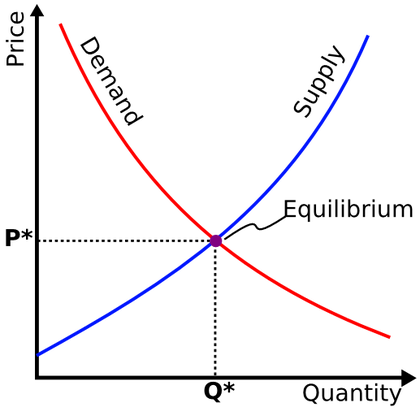

Price is the amount of money exchanged for a good or service. Interaction of supply and demand determines price. Price determines who acquires goods and services.

Incentives are things that incite or motivate. Incentives are used to change economic behavior. EX: Sales are incentives to get people to buy certain items and/or shop in your store.

Supply and demand: Interaction of supply and demand determines price. Demand is the amount of a good or service that consumers (shoppers) are willing and able to buy at a certain price. Supply is the amount of a good or service that producers (businesses) are willing and able to sell at a certain price.

Production is the combining of human, natural, capital, and entrepreneurship resources to make goods or provide services. Resources available and consumer preferences determine what is produced.

Consumption is the using of goods and services. Consumer preferences and price determine what is purchased and consumed.

Scarcity is the inability to satisfy all wants at the same time. All resources and goods are limited. This requires that choices be

made. EX: A baker may only have enough dough to make bread, croissants, or bagels, and must decide which option is best.

Resources are factors of production that are used in the

production of goods and services. Types of resources are natural (trees, oil), human (workers), capital (tools, cash registers), and entrepreneurship (business owners, inventors).

Choice is selection of an item or action from a set of possible alternatives. Individuals must choose or make decisions about desired goods and services because these goods and services are limited.

Opportunity cost is what is given up when a choice is made—i.e., the highest valued alternative is forgone. Individuals must consider the value of what is given up when making a choice. EX: If you want to buy a book and a game, but you only have enough for one, the one you give up is the opportunity cost.

Price is the amount of money exchanged for a good or service. Interaction of supply and demand determines price. Price determines who acquires goods and services.

Incentives are things that incite or motivate. Incentives are used to change economic behavior. EX: Sales are incentives to get people to buy certain items and/or shop in your store.

Supply and demand: Interaction of supply and demand determines price. Demand is the amount of a good or service that consumers (shoppers) are willing and able to buy at a certain price. Supply is the amount of a good or service that producers (businesses) are willing and able to sell at a certain price.

Production is the combining of human, natural, capital, and entrepreneurship resources to make goods or provide services. Resources available and consumer preferences determine what is produced.

Consumption is the using of goods and services. Consumer preferences and price determine what is purchased and consumed.

Supply and Demand

SOL 11b: What are the basic economic questions all societies must answer? What are the basic characteristics of traditional, free market, command, and mixed economies? How does each type of economy answer the three basic questions?

Every country must develop an economic system to determine how to use its limited productive resources.

The key factor in determining the type of economy a country has is the extent of government involvement.

The three basic questions of economics

· What will be produced?

· Who will produce it?

· For whom will it be produced?

Each type of economy answers the three basic questions differently.

Characteristics of major economic systems

· No country relies exclusively on markets to deal with the economic problem of scarcity.

Traditional economy

· Economic decisions are based on custom and historical precedent (how it's always been).

· People often perform the same type of work as their parents and grandparents, regardless of ability

or potential.

Free market economy

· Private ownership of property/resources (people, not the government, own them)

· Profit motive

· Competition

· Consumer sovereignty

· Individual choice

· Minimal government involvement in the economy

Command economy

· Central ownership (usually by government) of property/resources

· Centrally-planned economy

· Lack of consumer choice

Mixed economy

· Individuals and businesses are owners and decision makers for the private (non-government) sector.

· Government is owner and decision maker for the public sector.

· Government’s role is greater than in a free market economy and less than in a command economy.

Most economies today, including the United States, are mixed economies.

The key factor in determining the type of economy a country has is the extent of government involvement.

The three basic questions of economics

· What will be produced?

· Who will produce it?

· For whom will it be produced?

Each type of economy answers the three basic questions differently.

Characteristics of major economic systems

· No country relies exclusively on markets to deal with the economic problem of scarcity.

Traditional economy

· Economic decisions are based on custom and historical precedent (how it's always been).

· People often perform the same type of work as their parents and grandparents, regardless of ability

or potential.

Free market economy

· Private ownership of property/resources (people, not the government, own them)

· Profit motive

· Competition

· Consumer sovereignty

· Individual choice

· Minimal government involvement in the economy

Command economy

· Central ownership (usually by government) of property/resources

· Centrally-planned economy

· Lack of consumer choice

Mixed economy

· Individuals and businesses are owners and decision makers for the private (non-government) sector.

· Government is owner and decision maker for the public sector.

· Government’s role is greater than in a free market economy and less than in a command economy.

Most economies today, including the United States, are mixed economies.

SOL 11c: What are the essential characteristics of the United States economy?

The United States economy is primarily a free market economy; but because there is some government involvement it is characterized as a mixed economy.

Government intervenes in a market economy when the perceived benefits of a government policy outweigh the anticipated costs.

Characteristics of the United States economy

· Markets are generally allowed to operate without undue interference from the government. Prices are

determined by supply and demand as buyers and sellers interact in the marketplace.

· Private property: Individuals and businesses have the right to own real and personal property as

well as the means of production without undue interference from the government.

· Profit: Profit consists of earnings after all expenses have been paid. For example, if the resources to make a table cost $100.00, and the furniture store sells it for $300.00, the business has made a profit of $200.00.

· Competition: Rivalry between producers and/or between sellers of a good or service usually results in

better quality goods and services at lower prices.

Consumer sovereignty: Consumers determine through purchases what goods and services will be produced. Government involvement in the economy is limited. Most decisions regarding the production of goods and services are made in the private sector.

Government intervenes in a market economy when the perceived benefits of a government policy outweigh the anticipated costs.

Characteristics of the United States economy

· Markets are generally allowed to operate without undue interference from the government. Prices are

determined by supply and demand as buyers and sellers interact in the marketplace.

· Private property: Individuals and businesses have the right to own real and personal property as

well as the means of production without undue interference from the government.

· Profit: Profit consists of earnings after all expenses have been paid. For example, if the resources to make a table cost $100.00, and the furniture store sells it for $300.00, the business has made a profit of $200.00.

· Competition: Rivalry between producers and/or between sellers of a good or service usually results in

better quality goods and services at lower prices.

Consumer sovereignty: Consumers determine through purchases what goods and services will be produced. Government involvement in the economy is limited. Most decisions regarding the production of goods and services are made in the private sector.

Private Property

|

Competition

|

Consumer sovereignty

|